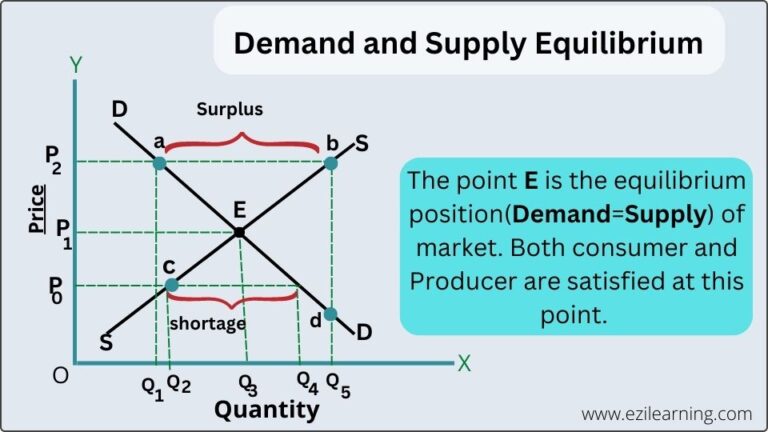

Explain the law of supply and demand?

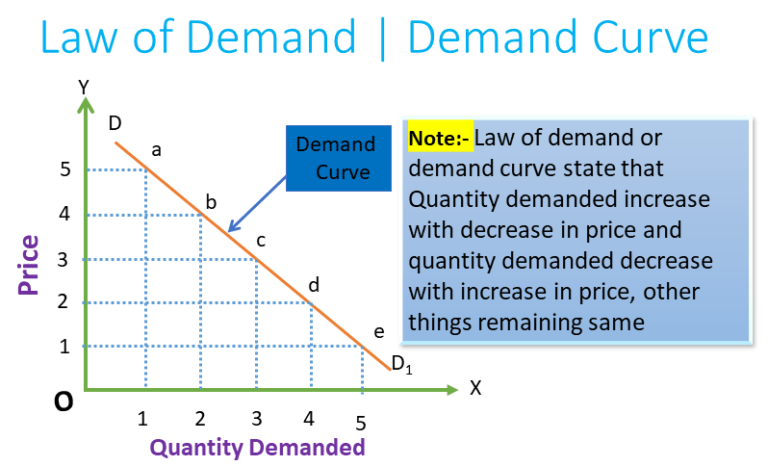

Introduction The Law of demand refers that when the price increases then the quantity demanded of that commodity decreases and vice-versa, other things remain the same. There …

Introduction The Law of demand refers that when the price increases then the quantity demanded of that commodity decreases and vice-versa, other things remain the same. There …

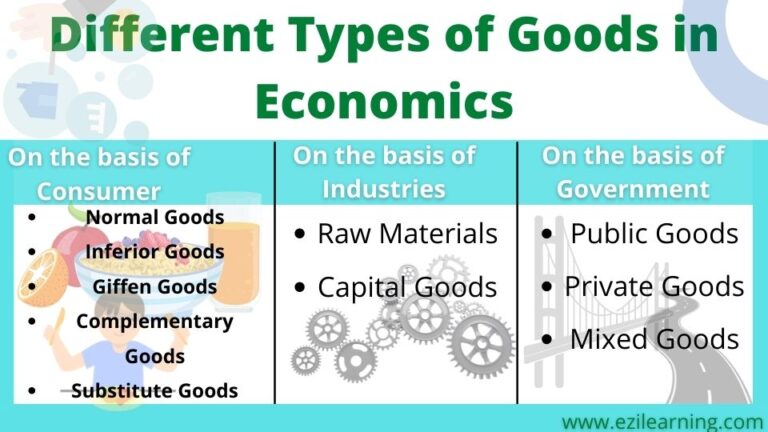

Introduction When economists have been studying the market economy, they saw that different goods react distinctively when there is a change in economic variables(price, income, …

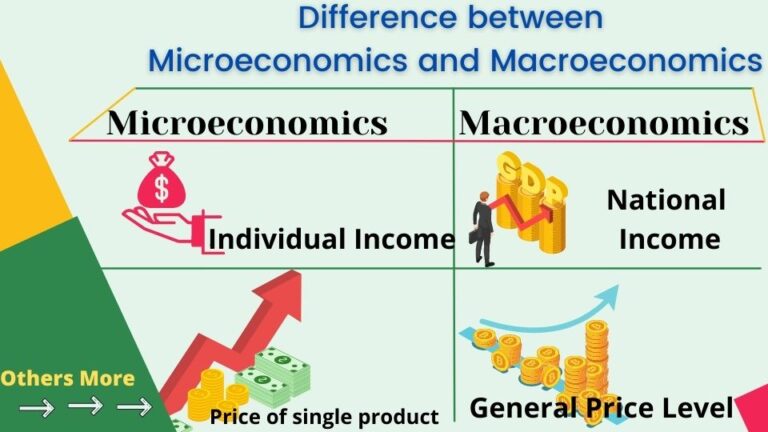

Introduction to Microeconomics and Macroeconomics The term microeconomics and macroeconomics were coined by Ragnar Frisch in 1930. He classified economics into two branches; Microeconomics and …

We are discussing here the important question answer of microeconomics from an exam point of view. But note that it is only a short question …

What is Cross elasticity of Demand? [su_highlight background=”#ffdb99″ color=”#0c0b0b”]Cross elasticity of demand is a measure of how much the quantity demanded of good changes, responds …

Definition: The income elasticity of demand measures how the quantity demanded changes as consumer income changes. Economists compute the income elasticity of demand as the …

Introduction: The concept of elasticity of demand was first introduced by the classical economists A.A. Cournot and J.S. Mill. Later on, neo-classical economist Alfred Marshall …

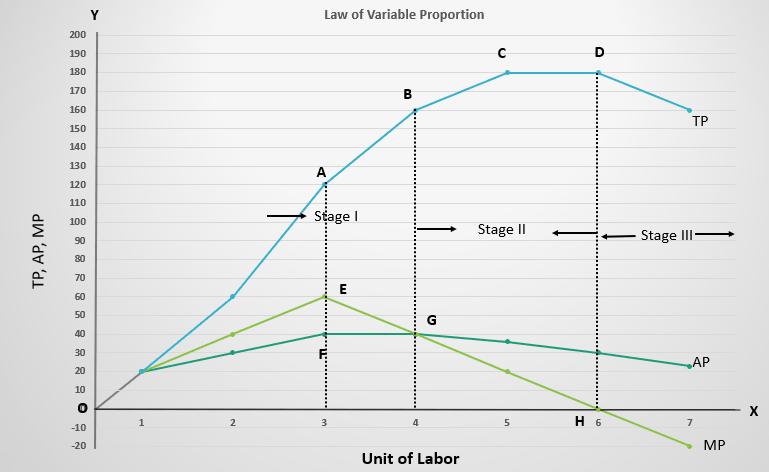

Table of Contents Definition of Total Product (TP) In economics, Total product is the output produced by the firm within the given period of time …

Introduction The law of variable proportion was first introduced by the economists like Joan Robinson, Alfred Marshall, Benham, etc. This law only applies to short-run …

Concept of Demand Demand refers to the wiliness and ability of consumers to purchase goods and services from the market at various prices per period …