Importance of Accounting Concept and Principle

Accounting concepts and principles are the guidelines and rules which maintain the accounting standard of recording transactions. These principles and concepts and are known as GAAP (Generally Accepted Accounting Principles). The basic objective behind the formulation of GAAP is to make all financial reports reported by any firm from any nook and corner of the world comparable to each other.

There is no universal GAAP standard, it may differ from one geographical location or industry to another. In the United States, the Securities and Exchange Commission (SEC) mandates that financial reports adhere to GAAP requirements. The Financial Accounting Standards Board (FASB) stipulates GAAP overall and Governmental Accounting Standards Board (GASB) stipulates GAAP for state and local government. Publicly traded companies must comply with both SEC and GAAP. But many counties of the world adopted IFRS (International Financial Reporting Standards. It was designed for the framework of public companies to record their transactions.

Full-Form

The rules maker – GAAP (Generally Accepted Accounting Principles)

The rule enforce – FASB (Financial Accounting Standard Board)

The CPA (Certified public accountant) regulators – SEC (Securities and exchange commission)

The rules – AICPA (American Institute of a certified public accountant)

Accounting Concept and Principle

Accounting Concepts or principles define as those basic assumptions or conditions upon which the science of accounting is based. The following are some important accounting concepts and principles.

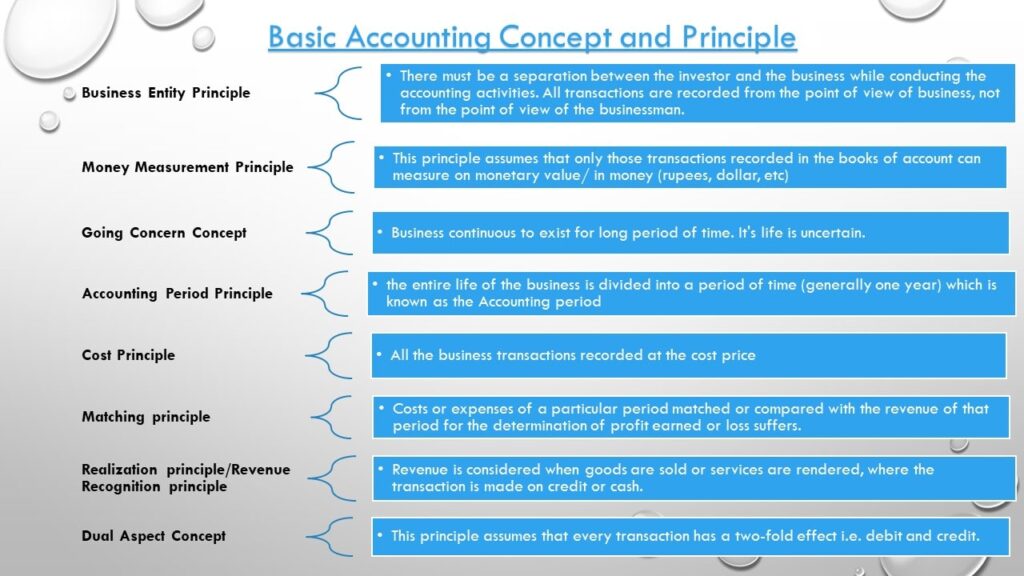

Business Entity Principle of accounting

There must be a separation between the investor and the business while conducting the accounting activities. All transactions are recorded from the point of view of business, not from the point of view of the businessman. We supposed that business is the artificial person and businessman is a natural person who makes an investment in it. So, they treat as creditors of business whose primary interest is of the safety of their interest and regular return.

Money Measurement Principle of accounting

This principle assumes that only those transactions recorded in the books of account can measure on monetary value/ in money (rupees, dollar, etc). In other words, It means that non-monetary transactions not recorded in books of account. Some non-monetary transactions are; strike, efficiency quality of management, employee motivation towards work, etc.

Going Concern Concept of accounting

Business continuous to exist for long period of time. It’s life is uncertain.

Accounting Period Principle of accounting

Business is a continuous process. Its life is indefinite. Thus, the entire life of the business divided into a period of time (generally one year) called the Accounting period. At the end of the accounting period; financial statements ( i.e. Income statement and Balance sheet) prepared to know the profitability and financial position of the business.

Cost Principle of accounting

All the business transactions recorded at the cost price. All the assets recorded in the at cost price (cost price:- the price at which assets are acquired). Market price does not play any role in these entries.

Matching principle of accounting

This concept is based on the accounting period concept. Costs or expenses of a particular period matched or compared with the revenue of that period for the determination of profit earned or loss suffers. Due to this concept; adjustments entries made to calculate profit or loss of the particular period likewise; outstanding, prepaid, written off, etc.

Realization principle/Revenue Recognition principle

Revenue is considered when goods are sold or services are rendered, where the transaction is made on credit or cash. Examples; sales on approval not recorded as revenue until approved by customers.

Dual Aspect Concept

This principle assumes that every transaction has a two-fold effect i.e. debit and credit. It means every transaction recorded in two places or accounts. For example; purchases of goods have two aspects i.e. i) receiving goods and ii) giving cash. Thus, the duality concept commonly expresses in terms of fundamental accounting equation;

Assets=Capital + Liabilities

Accounting Convention

Accounting Convention define as those customs or traditions which guide the accountant while preparing the accounting statement.

Materiality Principle

Only those transactions should be recorded which are materials or relevant for the determination of income of the business or which affect the managerial decisions. Materiality refers to the large sizes of amounts a relatively large amount is material while relatively small amounts are non-materials. For Example; purchases of stationery recorded as expenses even if the stationary (suppose calculator) runs from one accounting period to another.

Conservatism Principle

If it is possible of any loss in the future then the manager should make provision to bear the losses in the future. This convention states that “Anticipate no profit but provide for all possible losses”. Because of these conventions, provision is made; likewise provision for doubtful debts, provision for depreciation, etc.

Full Disclosure Principle

Full Disclosure conventions state that all the relevant and materials information of financial statements should be fully disclosed. So, that manager can take good decisions. Full discloser means that there should be full, fair, and adequate discloser of accounting information, non information should be hidden.

Consistency and Comparability Principle

This convention says that all financial transactions recorded on the same concept/assumption/ principles and policy. It facilitates, to compare the organization from one accounting period to another accounting period. If the concept or policy for entering the financial transaction changed, then statements should not show the correct profitability and financial position of the business.

For example; if depreciation on fixed assets is made on the straight-line method in the first year and diminishing in the second year. Then the financial statement doesn`t show the correct position of firms.